Guide to Invoice Financing and Factoring

Guide to Invoice Financing and Factoring

How to use receivables to get quick cash

Invoice Financing/Factoring Overview

Invoice financing and factoring are two similar means for businesses to leverage their accounts receivables to obtain a capital infusion. Because receivables are used as collateral for the financing, the products are only available for businesses that do B2B or B2G (government) sales

These loans can act as a means to bridge cash flow gaps for businesses that are waiting on payment for goods or services, especially those with longer payment terms. The most common industries include distributors and wholesalers, manufacturers, oilfield and gas, trucking and freight, staffing agencies, construction and government contractors.

Since the loan is secured by a tangible asset (invoice) it may be easier to qualify vs traditional lending options. Therefore, these products are often utilized by businesses without well established credit or who may be experiencing a time crunch.

Many borrowers enjoy the speed and relative ease of funding with these products. On the flip side, capital borrowed can be much more expensive than a traditional business loan acquired from a bank or other online lender. With very short payback times, APRs can go well into the double digits.

Invoice Financing

Invoice financing, also referred to as accounts receivable financing, is akin to a loan that utilizes assets as collateral. The unpaid invoice is presented to the lender, let’s use $100,000 as a nice round hypothetical number, the lender may be willing to provide up to $100k but typically much less, in most cases closer to $80k.

The lender will charge a processing fee in addition to a factor rate, which is similar to an interest rate on a standard loan, on the borrowed amount. These factor rates are typically applied on a weekly or even daily basis, which can add up to APRs of 25% or (significantly) higher.

Once the invoice is paid, the business must pay back the loan. If the invoices are paid off in 1 week, then the interest paid to the lender may be negligible. However, if the payment takes longer than expected, interest will accumulate making this a potentially expensive way to borrow capital.

Let’s say you receive $80k for your $100k in receivables with a 1% processing fee and a 1.5% weekly factor fee. Your invoice gets paid 5 weeks later, which means you end up paying $6,800 in interest/fees on your $100k in receivables (oof!)

As with most loans, a businesses’ credit and owner’s credit can increase or decrease the fees and interest a lender is willing to provide. Additionally, the business responsible for paying the invoice will also be assessed by the lender to try and determine likelihood of timely repayment, which can impact rates. However, an invoice from a business without a proven track record of payment may not be eligible for invoice financing.

With invoice financing, the business is still responsible for collecting payment for the invoice and paying back the lender once the invoice is repaid. This is advantageous to the borrower as it allows them to maintain control over the relationship with their customers. The last thing many businesses want is some pesky company blowing up their customers trying to collect on a loan.

Invoice Financing Pros

Quick cash (in as little as 24 hrs)

Lower eligibility requirements

Maintain control over the customer relationship vs factoring

Invoice Financing Cons

High costs (fees and rates)

May come with hidden fees (read your contracts!)

Unpredictability of cost as it’s dependent on how long it takes to collect invoice payment

Limited to B2B businesses

What Lenders Offer Invoice (A/R) Financing?

Invoice financing is not a common product as most businesses opt for factoring or a traditional business loan. Thus, there aren’t as many lenders in the market.

1st Commercial Credit

https://www.1stcommercialcredit.com/

Financing rates at .69%-1.59% (typically on a weekly basis)

Eligibility

Amounts from $10,000-$10,000,000

B2B invoices only

No financials required for loans up to $350k

Pros

No upfront, hidden, facility or audit fees

Funding in 3-5 working days

Maintain control over the customer relationship (vs factoring)

AltLine

https://altline.sobanco.com/

Rates are not clear

Eligibility

Amounts from $150,000-$5,000,000

B2B invoices only

Guarantee required

No time in business requirements, startups eligible

Pros

No credit checks

Bank lender so may be cheaper than alternative lenders

Maintain control over the customer relationship (vs factoring)

Cons

More complex structure, not as suitable for newer businesses

Invoice Factoring

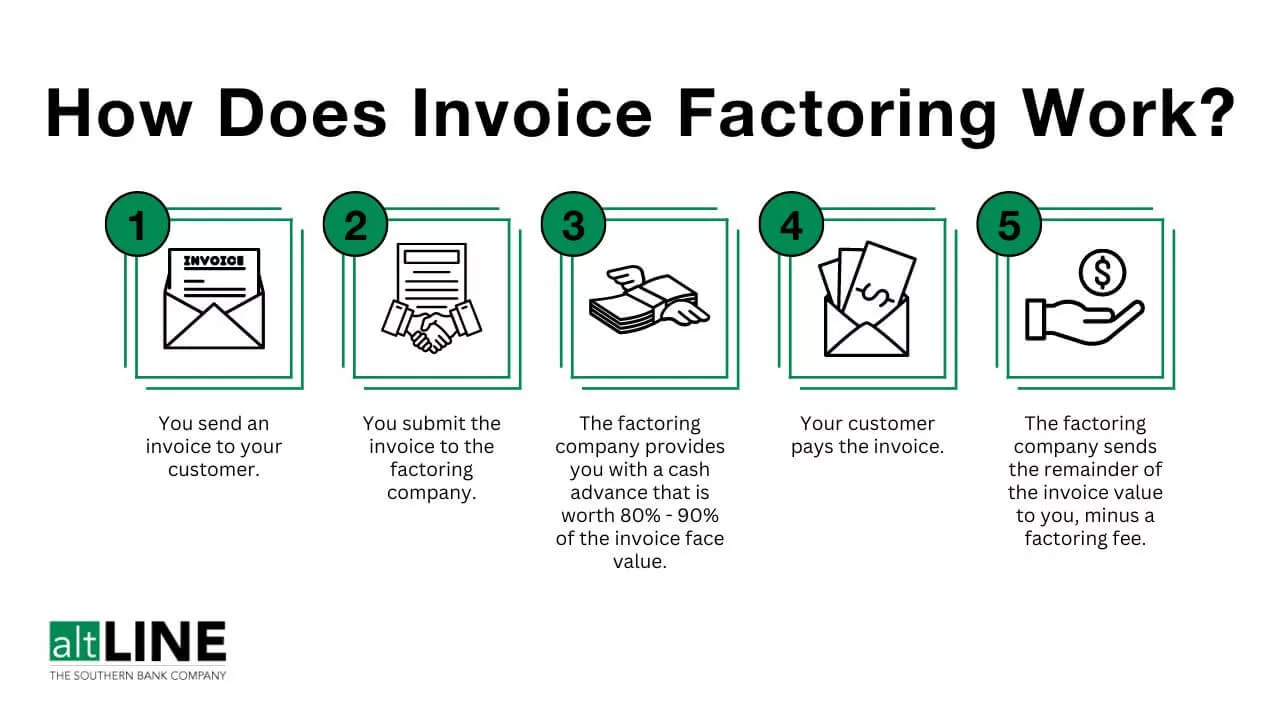

The primary difference in invoice factoring is that the factoring lender purchases the invoice outright from the business seeking capital. The lender then becomes responsible for collecting payment. Due to this structure invoice factoring is not considered a loan.

Factoring companies will ‘advance’ up to 100% of the invoice ‘face value’, but often less, and then collect directly from your B2B customer. Once the invoice is paid, they will remit the remaining amount less any fees. For example, if you want to factor $100k in invoices at a 90% advance rate and a 5% fee, you will receive $85,500 up front and the remaining $9,500 at time of payment.

When you sell your invoices, it’s important to note that your customer will receive a notice of assignment, which informs your customer that a third party is now responsible for collecting the invoice/receivables moving forward. Depending on the relationship with your customer, you may want to inform them in advance as a courtesy.

It’s important to note there are two main types of factoring that can impact the total cost of financing:

Recourse factoring means you have to buy back unpaid invoices but typically comes with lower fees.

Non-Recourse factoring means the factoring company incurs the liability of unpaid invoices but will come with higher fees.

Like invoice financing, the business responsible for paying the invoice will also be assessed by the lender to try and determine likelihood of timely repayment, which can impact fees. An invoice from a business without a proven track record may not be eligible for factoring.

Invoice Factoring Float

When payments are made via check or ACH, settlement doesn’t happen instantaneously (BiTcOiN fIxEs ThIs). The period of time for money to transfer from one bank account to another is called ‘float’.

In factoring, float or clearance days is the allowance for check clearance/payment settlement. Most factoring contracts will include a provision for float days, industry standard being 3 days but potentially up to 5 days. Float days are meant to protect lenders from bad checks.

This can have a negative impact on the borrower because the lender continues to accrue interest during the float period, which can sometimes knock you into a higher fee bracket leading to a potentially YUGE increase in borrowing cost.

ASK YOUR FACTORING COMPANY ABOUT THEIR FLOAT DAYS!

Invoice Factoring Pros

Quick cash (in as little as 24 hrs)

Easier application process vs other financing options

No impact on credit score since not a loan

Lower eligibility requirements

Invoice Factoring Cons

May come with hidden fees (read your contracts!)

Loss of control over the relationship with your customer

No guarantee of collection meaning your business may have to buy back invoices

What Lenders Offer Invoice Factoring?

FundThrough

https://www.fundthrough.com/pricing/

Terms

Receive up to 100% of invoice face value less the fee.

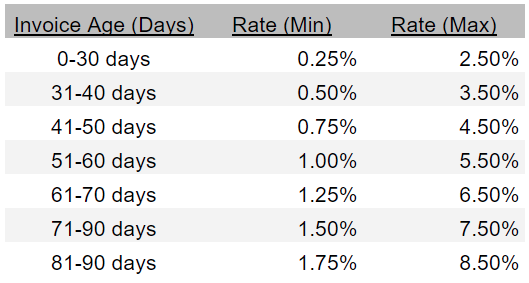

Fee of 2.75% per 30 days:

1-30 days, 2.75% fee

31-45 days, 3.75% fee

46-60 days, 5.5% fee

61+ days, 8.25%

Eligibility

Outstanding invoice of at least $100k in accounts receivables or invoice to one customer

B2B or B2G (government agencies) invoices

Invoices are for completed work (with an expected due date)

No construction or real estate

No explicitly liens on receivables

Pros

Advance rates up to 100% of invoice face value

No credit checks

Quick speed to funding (supposedly faster than most competitors)

Next-day funding

Works with a broad range of businesses and industries

Cons

Fees apply for early invoice payments

Invoices must be less than 90 days

Same-day funding requires additional fee

AltLine

https://altline.sobanco.com/

Terms

Receive 75-90% of invoice face value less the fee

Initial fee of .25%-2.5%

Incremental Fee of .25%-1% for every 10 additional days (see below)

Origination fee between $350-$500

Eligibility

Amounts from $30,000-$5,000,000

B2B invoices only

Guarantee required

No time in business requirements, startups eligible

Pros

No float days

No credit checks

Bank lender so may be cheaper than alternative lenders

Works with a broad range of businesses and industries

Cons

Funding not as quick as competitors

Same-day funding requires additional fee

Has an origination fee in additional to factor fees

Conclusion

Invoice financing and/or factoring can be a good option for businesses that have lots of outstanding receivables but need quick cash, or for businesses that aren’t eligible for more traditional sources of capital.

While these products tend to have a quicker payback period, they often come with higher APRs well into double digits. With relatively complicated contracts vs traditional loans, it’s important to ask your lender about fees and other contract terms that could increase the cost of borrowing.

Don’t get rugged out there, anons.

If you want to explore other SMB lending options, then check out our article on The Best Small Business Loan Options.

As always, this is not financial advice. For educational and entertainment purposes only.

Smash that share button and post on Twitter to spread the word of BTO.