Part 1: How to Get a Sales Job

Part 1: How to Get a Sales Job

At a FinTech SMB Lender

What are we going to cover?

Why get a sales job at an SMB lender?

Why listen to me?

What is an SMB Lender?

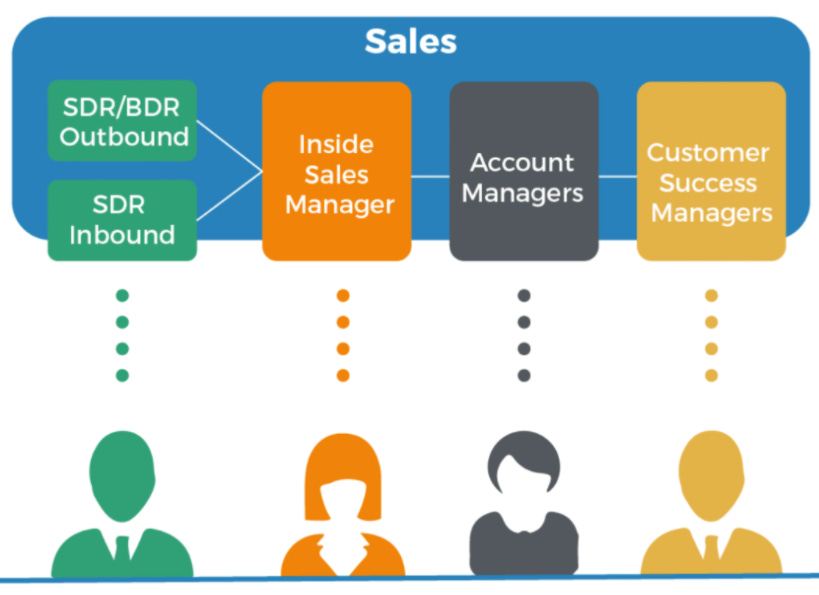

What types of sales positions are there?

What is the expected compensation?

Why should I get a sales job at an SMB lender?

If you’re part of the jungle, then you already know the plan:

Get a job in investment banking, SaaS sales, etc.

Build wifi money (e-com, affiliate marketing, consulting, etc.)

Invest in BTC (and ETH, LINK, etc.)

Don’t take it from me though. Go subscribe to Bull’s stack - bowtiedbull.substack.com

But, what if you’re still lost on landing the sales job (no experience) and have no idea where to begin with wifi money?

Get a sales job at an SMB lender.

How do you know this works and why should I listen to you?

Because I’m doing it right now. SDR to AM in less than a year.

Biggest month was $20k base + commission (mostly commission).

I don’t say this to brag but rather to impress upon you the opportunity.

It ain’t sexy but it pays the bills.

Why an SMB lender?

1) Low barriers to entry

I have seen people with no prior sales experience land SDR positions with $60k-$70k OTEs and CRUSH IT.

What’s your excuse, anon?

If you have even a little sales or finance/banking experience, you can probably secure an Account Executive/Account Manager (AE/AM) position out the gate. Earnings are likely less than SaaS but that’s because you don’t have the experience and ASPs/margins are lower.

But, to be faaaaair, I’ve seen plenty of companies advertise SaaS worthy OTEs.

The trade off vs SaaS Sales is a potentially much quicker ramp time to AE/AM from SDR. 6-12 month ramp up times is common but I’ve seen Chad’s and Chadette’s get promoted in ~3 months (dependent upon business need).

Once you make it to AE/AM you should be making $100k+ if you are a top performer. I’ve even seen some OTEs as high as $200k-$300k. If OTEs aren’t that high at your company, stick it out until you can leverage your experience into:

A sales position at a SaaS company (seen’t it plenty of times)

Hold out for a leadership position

Jump ship to a competitor with higher OTEs

2) You get to talk to small business owners everyday

You’re probably like why do I care?

Well, if your end goal is wifi money then these conversations are INVALUABLE especially if you lack the network IRL. You will learn dozens of business models, both wifi and traditional brick and mortar. Additionally, part of the role often involves reviewing the SMB’s financials.

You’d be surprised how many 1-2 person companies are clearing $100k+ profit.

Pay attention, find out what’s profitable. Try to replicate at a small scale in your free time. Build and iterate until you are 2x your day job income.

What is an SMB Lender?

A small and medium business (SMB) lender is any institution that lends money to SMBs. There are many types of companies considered SMB lenders including banks, credit unions, governmental agencies, and non-traditional lenders. For the sake of this article, I’m referring to the non-traditional lenders often lumped together under the nebulous term of “FinTech”.

FinTech (financial technology) is a catch-all term referring to software, mobile applications, and other technologies created to improve and automate traditional forms of finance for businesses and consumers alike (Source).

Why focus on FinTechs?

Other than the fact that banks are zeroes, working at a bank has limited financial upside especially if you’re working with SMBs. My buddy spent 3+ years at a bank and MAYBE cleared $65k a year after bonuses.

Unless you’re going into investment banking, don’t go the bank route.

Why do banks pay like crap?

SMB lending at a bank is an expensive endeavor and the returns are LOW because amounts are smaller than enterprise loans. Additionally, if you consider 7(a) loans currently yield 10-15% annually, banks aren’t earning a whole lot on the invested capital.

(Read my 7(a) deep dive article HERE)

For example, a $200,000 loan over 10 years at 10.50% will generate $124k in interest for the lender over those 10 years assuming no prepayment.

While you may be thinking $124k on $200k is a decent return, consider that stocks yielding 8% compounded annually would generate $232k in return.

Yes, stocks are more volatile but SMB lending is also very risky and a handful of defaults will destroy the yield on your entire book. Shit happens.

Additionally, banks don’t do themselves any favors by having clunky processes with tons of documentation, extensive manual underwriting procedures, and often overpaid underwriters. With such inefficient processes, an underwriter can only handle a couple files at a time making the whole undertaking an expensive venture.

Why do FinTechs pay better?

I should start by saying it depends on the position. But, as the title of this article states, I'm focusing on sales.

Largely, the value proposition of FinTechs is that they’ve streamlined the underwriting process by automating a lot of the credit decisioning using their fancy models and “technology”, which is supplemented with cheaper operational support.

With more efficient underwriting and operations compared to the banks, the name of the FinTech lending game is VOLUME.

Unlike banks, FinTech lenders don’t have a giant pool of depositors, credit card users, or other-services customers from which to obtain SMB loan clients. Therefore, these lenders must market like crazy and convert as many applications through the funnel as possible.

This is where the sales team comes in.

With such a big focus on customer acquisition and funnel conversions, FinTech lenders are willing to pay more for sales reps (and marketers but I’ll let BowTiedCoquito handle that one) vs similar roles at a bank.

What type of lender should you work at?

Hopefully by now I’ve convinced you that this path works and can be financially rewarding. Now you need to decide what type of lender to work for.

Within the FinTech space there are TONS of different lenders. However, for sake of simplicity I break them down into two buckets.

Direct Lenders

Marketplaces/Brokers

Direct Lenders underwrite, originate, and service their own loans (similar to a bank). Direct lenders can be either a balance sheet lender or a P2P lender.

Balance sheet lenders hold the loans on their books and incur any risk of default, just like a bank.

P2P Lenders connects borrowers that need loans with investors that want to invest in fixed income assets (SMB loans). The P2P lender does the customer acquisition, underwriting, servicing, etc. while the investor collects the yield from the loans. The P2P lender funds its operations by collecting fees from the borrower and/or lender for facilitating the loan.

A benefit of working at a direct lender is that you will likely have only a few products to sell so you can quickly become a subject matter expert. Less products to sell often means a quicker ramp up but could limit your ability to close any one customer. Borrowers often have a specific product in mind and if yours isn’t the right fit they’ll quickly go to a competitor.

There’s also a higher likelihood that you will believe in the product you're selling as there is a lot of trash out there (MCAs). This may seem inconsequential to a newbie but anyone who has been in sales long enough understands how paramount it is to believe in the product you are selling.

Companies include: Bluevine, Fundbox, Funding Circle, Kabbage, Ondeck, and many others.

Marketplaces/Brokers don’t have any of their own products to sell but simply connect prospective borrowers with direct lenders.

Marketplaces tend to be larger, more established companies that work with dozens of different direct lenders. They largely cover the entirety of the SMB FinTech lending space selling most types of products. You can read about the different product types HERE.

Brokers are typically smaller companies, often 1-2 person shops that work with only a handful of different lenders and often focus on one or two product types (equipment loans, MCAs, etc.)

A benefit of working at a marketplace or broker is that you will be exposed to many different product types.

I know I know… I said the opposite was also a benefit of being a direct lender. As with most things in life there are both positives and benefits, it simply matters how you frame it.

When you work at a marketplace/broker, you can sweep the entire industry to find your borrower the best fit product, often increasing the likelihood you can close the deal.

However, you may be expected to sell trash products with APRs as high as 100%. These high rate products often have the highest commissions so if you’re thinking you won’t be compromised, well… I doubt it.

Personally, I don’t support these high rate products as they often harm SMBs and my goal is to help. But, you do you , anon.

Companies include: Fundera, Lendio, NAV, and many others.

What about compensation?

Now let’s get into what you all really care about.

Compensation is ultimately a crap shoot. In my experience most lenders will have uncapped commissions. The market for quality salespeople is too competitive in the US and many of these lenders fancy themselves as Fin-TECHNOLOGY companies so need to keep compensation enticing enough to attract a decent level of candidate.

What matters most is OTEs and how many reps are hitting those OTEs.

$250k advertised doesn’t mean anything if very few reps are actually achieving those numbers.

If you make it to the later stages of the interviews, make sure you have an open and honest conversation about comp with the hiring manager. You should also review glassdoor.com and reach out to any current/past sales reps.

But, like any traditional sales organization, the biggest factor for comp will be the level of your role and corresponding experience.

SDR roles are more junior and will therefore have lower OTEs ($50k-$75k)

AE/AM roles are the next step up in the sales org and come with a higher expectation of experience and compensation ($80k-$250k)

What type of role should I go for?

It depends on your experience.

If you have little to no sales or lending experience you are likely going to have to settle for a Sales Development Representative (SDR) or similar position.

If you’re a sales chad with a couple of years of sales and/or lending/banking experience, it’s completely reasonable to immediately go for an Account Executive or Account Manager (AE/AM) or similar position.

What is an SDR?

SDRs, or similar positions, are at the top of your sales funnel. Often, these positions are trying to convince prospective businesses to apply for a loan. The true nature of the role will vary by company.

There are typically two types of SDR positions, outbound and inbound.

Outbound SDRs, sometimes called a Business Development Representative, as the name implies are calling out to prospective businesses. These may be businesses that have never interacted with your company before, they may be people who have received some form of marketing, or they may be prior clients.

Typically, the need for capital has not yet been identified with these businesses. The primary responsibility of an outbound SDR is to find businesses with a need or paint point and bring them into the funnel by showing the business how your product (loan) can be a solution. Common pain points include: slow paying customers, slow or stagnate growth in revenue or profits, inability to find/hire quality employees, among many others.

I consider this to be a ‘true’ sales role and similar to many SaaS SDR positions. It’s a slog (I’ve done it) and not for everybody but will teach you many valuable skills. Most importantly, perseverance in the face of rejection. Cut your teeth in this position and you’ll have the skills to be an SDR at any company or an AE/AM at your current company.

Inbound SDRs are interacting with prospective businesses that have shown a higher level of interest in your company’s solutions. These businesses may have contacted your company directly after searching for solutions or receiving marketing materials, they may have submitted an inquiry or even started an application but did not complete it.

This tends to be an easier sale as the borrower has already identified a need or pain point and is actively seeking a solution. The role consists more of educating the borrower on your product and its features/benefits and then trying to get an initial application completed.

What is the expected compensation for an SDR?

I’ve seen positions paying as little as $20/hour with little to no commission. I also know of companies with OTEs around $65k-$70k.

Do your research and know that competition will be higher at companies with higher OTEs.

What is an AE/AM?

The name of this position in the SMB lending industry feels like a misnomer to me.

Its closest counterpart in the traditional banking industry is known as a “Loan Officer”. In the FinTech space I’ve seen it called many things including: Account Manager, Account Executive, Funding/Loan Specialist, Funding/Loan Consultant, and a myriad of other titles to obfuscate the role and responsibilities of this position.

At the end of the day, it’s sales.

For the sake of this article, I’m going to continue referring to this position as an AE/AM but know that it encompasses any and all monikers listed, or not, above.

The main responsibility of an AE/AM is to walk businesses through the loan application process. This includes:

Being the main point of contact for prospective borrowers

Educating business owners on the loan requirements and terms

Educating business owners on the lending industry and company’s fit

Doing basic discovery - asking questions to understand the business and their funding needs

Collecting required information and documentation for underwriting; ensuring said documentation is accurate

Acting as the liaison between the borrower and underwriters (if applicable - some lenders have darn near fully automated credit decisioning)

Communicate the loan terms to the business owner and convince them to accept

It’s about as order-taking as a ‘sales’ position can get. However, the best know how to influence the business owner’s decision making process by implementing many different sales techniques.

Perhaps one day I’ll write an article on this but for now I suggest you follow BowTiedSalesGuy.

Important Note: In most cases these positions are inbound meaning the applications quite literally fall in your lap through your marketing team’s efforts. You’ll get assigned new applications in whatever sadistic way your company chooses.

However, some companies may expect you to call out to cold leads or even warmer prospects with some knowledge of your product and/or need for funding.

There are often many other sales roles within a FinTech lender where you aren’t working directly with prospective borrowers. As with any job, make sure you fully understand the job description.

What’s the expected compensation for an AE/AM?

By now you should know what the answer is going to be… it depends.

Largely, it depends on your experience and the company you work for.

If your company’s OTEs aren’t ~$100k then you need to work harder or find a different company to work for. I see job postings almost every week with $100k+ OTEs.

Refer to my Substack articles with a list of lenders and their career pages HERE and HERE, go through them every week (or better yet every day) to find new postings. For funzies, and because I’m feeling generous, here’s a couple quick examples:

Balboa Capital - Sales Manager

https://www.balboacapital.com/careers/

Bluevine - Partner Account Executive

https://www.bluevine.com/careers

Funding Circle - SDR

Conclusion

Hopefully by now you realize I’m not bullshitting you.

But hopefully, you have also realized the wide range of compensation and the corresponding ranges in experience.

There is a role out there for anyone who wants to go this route. You just have to go out there and earn it.

At this point you should understand:

Why you should get a sales job at a FinTech SMB lender

Why I’m qualified to provide any info on the subject

What an SMB lender is

What the different roles, responsibilities, and compensation ranges are

If you haven’t already, make sure to subscribe to my Substack so you don’t miss Part 2 of How to Land a Sales Job at an SMB Lender where we’ll cover how to land the job, including:

Understanding your target company

How to write your resume

How to nail the interview

What you should expect and do in the first 90 days

As always, this is not financial advice. For educational and entertainment purposes only (do we really need to say this every time?).

-BTO