What Are Business Term Loans?

What Are Business Term Loans?

A guide to term loans for SMBs

What are Business Term Loans?

Business term loans are a lump sum of capital lent to businesses for a variety of uses. The payback period (term) is a set period with payments required on a predetermined schedule. Payments can be daily, weekly, or monthly as determined by the lender.

Business term loans can be used for a myriad of purposes including cash flow, long-term investments, debt consolidation, etc. However, you will want to check with your lender if there are any restrictions.

Loan Amounts

The amount of capital that can be accessed via a business term loan varies by institution and the business requesting the loan. Typically, amounts range from $5,000 to $5 million. Most lenders have restrictions in place to prevent overleveraging their borrowers such as loan to revenue or loan to cash flow ratios, similar to debt to income ratios in consumer lending.

Interest Rates

Interest rates will vary by lender, with traditional banks, credit unions, and the Small Business Administration (SBA) often offering the lowest Annual Percentage Rates (APRs). Rates at these institutions are typically anchored to the prime rate +/- premium depending on the creditworthiness of the business. More risky businesses will have rates above prime, less risky businesses closer to prime (duh).

Interest rates on business term loans can be either variable or fixed but fixed rate products typically come with a higher initial interest rate than a similar variable rate product. This is due to something called interest rate risk, which you can learn more about in our SBA 7(a) post HERE.

What is the prime rate?

The prime rate is the most common benchmark used by banks to set interest rates for different lending products. Banks commonly, but not always, use the federal funds rate + 300 basis points to set the prime rate. Source.

Most non-traditional online lenders often charge higher interest rates than banks, which is usually offset by the speed at which they are able to underwrite and fund loans. Most non-traditional lenders can fund a new application in as little as a few days whereas banks typically take a few weeks to months.

These non-traditional lenders can also make offers to businesses that fall outside of the SBA and traditional bank’s stricter underwriting criteria.Different lenders will have different risk tolerances which will ultimately dictate the size of the loan, the interest rates, and whether or not an offer can even be made.

Amortization

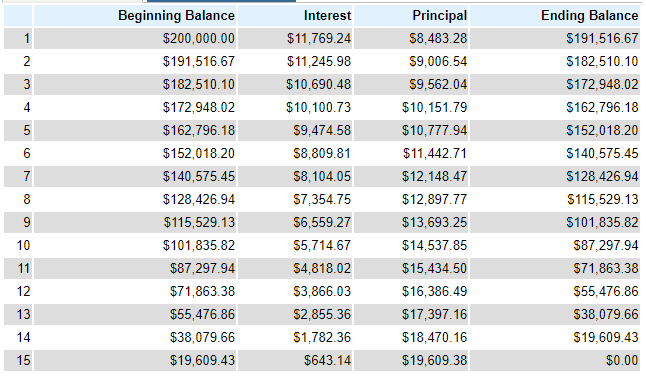

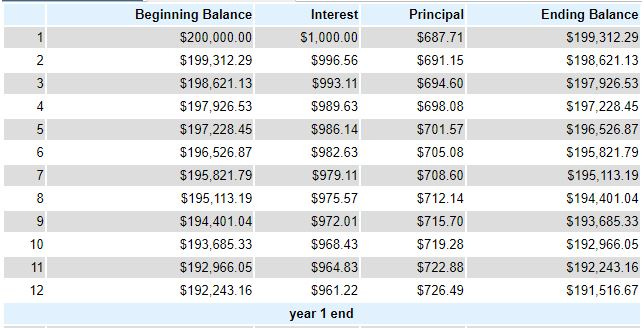

Many business term loans are structured as amortizing term loans meaning a portion of each payment goes towards principal and interest until the loan is paid in full. While not “front loaded” in the traditional sense like some loans, earlier payments have a larger portion applied towards interest than later payments. See the example amortization below.

The amount of each payment applied towards interest is a function of the loan’s interest rate and the outstanding loan principal.Thus, as payments are made, the overall principle of the loan decreases, so less of each payment is applied towards interest. Many car loans and mortgages utilize a similar payment schedule.

In the below example, you can see the first year of payments on a $200,000 loan over 15 years at 6%. You’ll notice that the first payment has $1,000 going towards interest, which can simply be calculated as the loan principal multiplied by the interest rate divided by payment frequency = $200,000*(6/12)= $1,000.

Prepayments

Prepayments are allowed by some lenders, though some may charge fees for doing so. Prepayments can be an excellent way to save money on the overall dollar cost of the loan if your business’s cash flow permits it. This is because any prepayment above and beyond the required payment is applied directly to the principal balance.

It’s important to note that due to the phenomenon described above, earlier prepayments are more advantageous than those made towards the end of the loan term.

What are the different types of Business Term Loans?

Short term:

Usually ranging from 6-24 months, can have monthly, weekly, or even daily repayment schedules. Most commonly sourced by non-traditional online lenders. These loans are best for quick infusions of cash for shorter term uses such as working capital to cover unexpected costs, payroll, or inventory.

Medium term:

Usually ranging from 2-5 years, can have monthly or weekly repayment schedules. Medium-term loans can be sourced from traditional lenders (banks, credit unions, SBA) and non-traditional online lenders. These loans can also be used for shorter term uses especially when accompanied with no prepayment penalties. However, with terms up to 5 years they tend to be more suitable for larger, more capital intensive projects with longer payback periods.

Long term:

Usually a term of 5+ years, typically with monthly repayments. While the overall cost of these loans is often higher, the lower monthly payments can easier on a business’s cash flow

Advantages

Fixed periodic payments allows businesses to forecast their debt servicing needs and required cash flow over the entire term length, assuming they are in a fixed rate product.

Able to access large sums of capital and pay it back over a longer period of time. Since businesses receive a lump sum up front, they can use it for a variety of reasons including projects that require large upfront investments with longer payback periods (depending on the term length).

Build business credit when you make on time payments as many lenders report to one or multiple business credit bureaus (Dun & Bradstreet, Equifax, and Experian). Many smaller, newer businesses don’t have business credit or aren’t even aware of its existence. Building business credit can help with better loan terms in the future, similar to how personal credit works.

Disadvantages

Only good for one time use unlike a line of credit or other revolving vehicle that allows continuous access to funds as you make payments.

Collateral, a UCC filing, or a personal guarantee may be required depending on the type of loan and/or institution you receive the loan from. Most non-traditional lenders require a UCC-1 filing and/or a personal guarantee to secure the loan. Whereas most banks or other asset based lenders will require collateral to secure the loan.

Hard to qualify for versus shorter term loans. Banks and credit-unions are the dominant provider of term loans, making them difficult to obtain. While non-traditional lenders often have easier requirements, they typically require strong business and/or personal financials to qualify.

What are the eligibility requirements?

While different lenders have varying risk tolerances, they all use similar criteria to underwrite a loan with some nuance. Some of the factors term loan lenders look for are:

Personal credit score - You may be thinking why do they care about my personal credit for a business loan? However, if you run your personal finances like crap, it’s like you run your business finances like crap

Business credit score - Similar to personal credit. Check your score through the 3 major bureaus: Dun & Bradstreet, Equifax, Experian

Business financials including revenue, profit, EBITDA, debt service coverage ratios, recent cash flow found in bank statements

Other factors - FinTech lenders like to think they’ve revolutionized underwriting with their fancy models so may have numerous other factors that go into their credit decisions.

What lenders offer business term loans?

Accion Opportunity Fund

https://aofund.org/

Minimum Requirements

Minimum Time in Business: 3 months

SSN or ITINs accepted

Not available in Montana, Nevada, South Dakota, Tennessee, or Vermont

Terms

Loan Amounts: $5,000-$100,000

Interest Rates: Starting at 5.99%

Term Lengths: 12, 24, 36, or 60 months

Payment Frequency: Monthly

Fees: 3.99%

Pros

Great for newer businesses and business owners that don’t have perfect credit. Looks at a number of factors and can make offers to businesses with promising business opportunities.

Cons

Not great for businesses looking to borrow more than $100,000 or individuals looking to start a business. Additionally, their product is not available in every state.

BHG Money

https://bhgmoney.com/

Minimum Requirements

Minimum Time in Business: 2 years

Minimum FICO: 660

Minimum Monthly Revenue: $6,250

Terms

Loan Amounts: $20,000-$500,000

Interest Rates: Not clear but you can likely expect APRs between 10%-20%

Terms Lengths: Up to 12 years

Payment Frequency: Monthly

Fees: Not clear but you can expect likely expect to fees between 2%-5%

Pros

Originally specialized in healthcare and other professional service related industries. Offers some of the longest term lengths outside of bank and SBA backed loans. Receive funds in as little as 3 days.

Cons

They don’t give a lot of information on their website and you must speak with a representative to submit an application.

Credibility Capital

https://credibilitycapital.com/

Minimum Requirements

Minimum Time in Business: 24 months

Minimum FICO: 650

Minimum Annual Revenue: $200,000

No bankruptcies in past 5 years

No current delinquencies exceeding $100,000

No unpaid/unsettled liens and/or judgements against the borrower or business

Not available in Nevada, North Dakota, South Dakota, or Vermont

Terms

Loan Amounts: $50,000-$500,000

Interest Rates: Starting at 9.49% for 5 year loans

Terms Lengths: Up to 5 years

Payment Frequency: Monthly

Fees: One time fee at closing but not clear on amount

Pros

Offers both a term loan and a business line of credit with some of the most competitive interest rates on their term loans in the alternative lending space. They also have no prepayment penalties.

Cons

Not for new businesses and term lengths cap out at 5 years.

Funding Circle

https://www.fundingcircle.com/us/

Minimum Requirements

Minimum Time in Business: 2 years

Minimum FICO: 660

No personal bankruptcies last 7 years

Terms

Loan Amounts: $25,000-$500,000

Interest Rates: 11.29%-30.12%

Terms Lengths: 6 months to 7 years

Payment Frequency: Monthly

Fees: One time fee at closing but not clear on amount

Pros

Available to businesses in all 50 states. Term lengths up to 7 years with no prepayment penalties. You can receive an approval in as little as 24 hours and funding as quickly as 1 business day.

Cons

Fees may be higher than other term loan lenders.

Conclusion

If you feel that a term loan is the best option for your business, then definitely check out the above lenders.

If you still have questions, feel free to shoot us a DM on Twitter @bowtiedoncilla.

If you want to explore other SMB lending options, then check out our article on The Best Small Business Loan Options.

As always, this is not financial advice. For educational and entertainment purposes only.

Smash that share button and post on Twitter to spread the word of BTO.