What is an SBA 7(a) loan?

What is an SBA 7(a) loan?

A deep dive into the SBA's flagship lending program

What we will cover:

7(a) Overview

Amortization

Interest Rates

Eligibility Requirements

Best Use Cases

Pros & Cons

Prepayment Penalties

SBA 7(a) Loans Overview

The 7(a) is the SBA’s flagship lending program offering SMBs loans up to $5M and payback periods up to 25 years for real estate or 10 years for non-real estate uses. Yes anon, you could get a $5M loan from the banks (zeroes) backed by the federal government. That’s gotta be darn near enough guacamole to buy Bull’s Twitter account and Substack.

Oh, and I know how the jungle largely feels about these two entities (banks and government) but if you can make them work for you, why wouldn’t you take advantage?

Credit: @bowtiedfarmer

The SBA 7(a) is typically structured as a fully amortizing term loan meaning a portion of each payment goes towards principal and interest with the loan paid in full on the last payment. For the term loan option borrowers receive a lump sum up front and make monthly payments until the loan is paid in full, just like your mortgage or car loan.

It’s important to note that amortizing terms loans, while not front loaded with interest like some interest only loans, do have a larger portion of each payment going towards interest at the beginning of the loan vs the end.

On an $800,000 loan over 10 years at 10.50% your payment would be ~$10,795

In year 1 your payments would look like this:

By year 10 your payments would look like this:

From calculators.net (source)

By the end of year 1 in a 10 year loan (10%) you’ve already paid 16% of the interest!

Due to this property of amortizing loans, you stand to save more in interest cost by making larger payments at the beginning of your term vs the end. This is because any prepayment above and beyond the monthly payment is applied to the principal, unless otherwise stated in the contract. Additionally, the amount of your payment applied towards interest is a function of the interest rate and outstanding principal.

Therefore, large prepayment early can drastically reduce the outstanding principal and the subsequent interest cost.

If you can afford it, make larger payments sooner rather than later. However, the 7(a) does have prepayment penalties. More on that later.

In addition to the 7(a) standard loans, the SBA offers several variations and offshoots of this product. You can learn more about the various options on the SBA’s site. Maybe one day we’ll do a deep dive into all of these. Subscribe to stay toon’d.

Interest Rates

SBA approved 7(a) lenders are comfortable offering lower interest rates than they might otherwise because the SBA (federal government) guarantees up to 85% of the loan principal. Meaning, if the borrower defaults then the lender can recoup a majority of the lent amount.

7(a) loans may come with variable or fixed rates depending on the lender and/or borrower preference. Importantly, fixed rate products come with higher interest rates, all else equal. This is due to the lender’s increased interest rate risk from locking in the rate.

What is interest rate risk?

Think of it this way - Interest rate risk is essentially the opportunity cost of missing out on an even higher return if rates were to increase (like they did in 2022). As a lender I may lock away my capital for 10 years earning only 10% but could have received 15% if rates increased and I waited to deploy capital.

On the flip side, as the borrower you also face risk from rising interest rates by opting for a variable rate loan. Let’s say you take out a variable rate loan of $250k over 10 years at 10.25%, your monthly payment will be ~$3,338. If the prime rate increases 5% 2 years later your payment will go up to ~$4,072.

Is your business prepared to shell out an additional $8,808 per year? Ideally, whatever project you’re using the funds for has started to generate a return but life and business doesn’t always work out that way, especially projects with longer payback horizons.

Taking out a fixed rate at a higher interest rate is like buying a hedge against rising interest rates. If rates were to quickly and dramatically decrease you could always refinance down to a lower rate.

It all depends on your risk tolerance, specific business situation, and to some degree your outlook on interest rates.

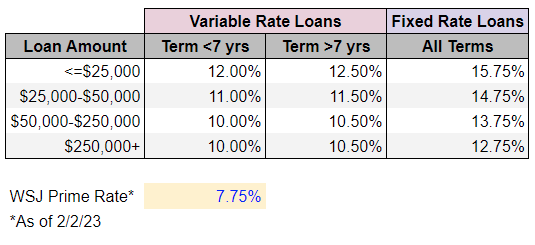

While interest rates are negotiated between borrowers and lenders they are not to exceed the SBA’s stated maximums (in reality they’re set by the lender). SBA maximums below.

As you can clearly see in the above table, fixed rates and longer term lengths have higher interest rates, all else equal. If you go the 7(a) route, make sure you have the interest rate conversation with your lender.

Eligibility Requirements

(1) Operate for profit

Can’t be a not-for-profit business or other ineligible business/industry type. Ineligible businesses include (but not limited to): those engaged in illegal activities, loan packaging, speculation, multi-sales distribution, gambling, investment or lending, or where the owner is on parole. See the full list of ineligible businesses on the SBA’s website.

(2) Be considered a small business, as defined by the SBA

This one seems like it should be pretty straightforward but leave it to the federal government to make it more complicated than is seemingly necessary. The SBA defines “small” differently based on your NAICS code (industry description). To make things even more complicated, depending on your NAICS code your business needs to meet either an annual revenue OR number of employees threshold (at least it’s not Twitter followers). You can see the entire list of NAICS codes and restrictions in the SBA’s Table of Small Business Size Standards.

Oncilla Note: There’s someone at the SBA with the title “Size Specialist”. I wonder if their supervisor is the “Size Lord”.

(3) Be engaged in, or propose to do business in, the U.S. or its territories

The business must be physically based in the United States and you must be doing business with the U.S. and its territories.

(4) Have reasonable owner equity to invest

Must show that you as the owner are investing your own time and money into the business. If you’re acquiring a business with the loan proceeds you must invest at least 10% of your own capital.

(5) Use alternative financial resources, including personal assets, before seeking financial assistance - otherwise known as “credit not available elsewhere”

Basically, the borrower must have tried to obtain funding from non-governmental sources but “the desired credit is unavailable to the applicant on reasonable terms and conditions” from non-governmental sources.

Oncilla Note: This one is kind of BS. In my experience a business can have an offer from another lender but still obtain an SBA 7(a) loan. Just say the interest rate is “too high” and it will probably pass muster for most 7(a) lenders.

(6) Be able to demonstrate a need for a loan

Pretty straight forward.

(7) Use the funds for a sound business purpose

Businesses must use the funds for an eligible purpose including but not limited to: acquire land, improve a site, purchase one or more existing buildings; convert, expand, or renovate one or more existing buildings; construct one or more new buildings; acquire and install fixed assets with a useful life of at least 10 years; inventory, supplies, raw materials, working capital, and/or refinancing certain outstanding debts (source).

(8) Not be delinquent on any existing debt obligations to the U.S. government

The federal government is ALWAYS going to get theirs. As this guy likes to say…

(9) Most lenders have their own, often stricter, eligibility requirements

If interested in a 7(a) loan you will need to discuss any additional eligibility requirements with your lender. The additional criteria I have seen include: positive EBITDA, strong debt service coverage ratios, FICO minimums, and revenue/earnings growth.

Best Use Cases

Per the above section on eligible use of funds, there are a lot of potential uses for a 7(a) loan. However, due to the more extensive application process, longer processing times, and the nature of a term loan product (ie. upfront sum of money with monthly payments up to 10/25 years) the product tends to be more advantageous for specific uses.

Why would you waste all of that time just trying to get the loan with no guarantee of approval for something like working capital or inventory that you can turn over in a few months and be stuck with a loan for 10 years? You’re better off getting a line of credit or something relatively shorter term with no prepayment penalties that you can pay off quicker.

Ideally, you would be utilizing these funds for a project that requires a large upfront sum with a longer, but relatively certain, payback period.

A great example is buying an existing business.

Let’s say Bull offers you a deal of a lifetime to buy his Twitter and Substack for $1M but you only have $200k in the bank. If acquiring a business with a 7(a) loan you will need to put at least 10% down but I’m assuming you’ve been following the BTB playbook and have some extra cheddar laying around.

Let’s also assume Bull’s assets are printing $100,000/year in net profit and growing 10% YoY

Simplified example, because math’s.

To make the purchase you put up your $200k and borrow the remaining $800k.

Monthly payments on an $800k loan at 10.5% over 10 years are ~$10,795 or $129,540 annually.

Your expected profit after 10 years would be $299k, a ~50% return on your initial $200k.

Not bad but might as well buy some $BTC.

Oncilla Note: This is a simplified example and doesn’t take into account SO MANY factors.

Unless you already own an existing business in the same or related industry it will be difficult to acquire a business as an individual.

As an individual, you will often need significant industry experience and some skin in the game to qualify. The SBA requires at least 10% down but potentially more.

This assumes you’re in the variable rate 7(a) product and rates don’t change (unlikely).

If we wanted to know the true expected return from this investment we would need to do some discounted cash flow analysis.

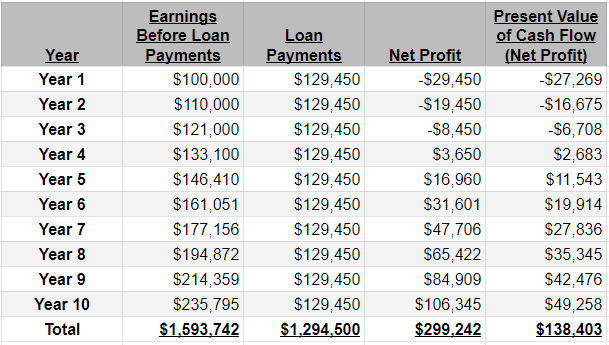

Screw it. Let’s do the DCF analysis. Here’s the 10 years assuming a conservative 8% discount rate (WACC).

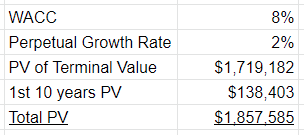

After year 10 we’ll assume earnings grow at 2% per annum with an 8% WACC. At this point the loan is paid in full so you receive the full earnings of $235,795 plus the 2% annual growth. Then we need to discount it to get the present value 11 years out. Based on those assumptions we get the following:

If you believe you can grow Bull’s profit/cash flow by 10% for the next 10 years and then continue growing it in perpetuity at 2% then you would get a ~$1.9M present value (PV) after the cost of the loan. Not bad.

Pretty sure those math’s are right… Been 10 years since my last finance class.

Anyways, hopefully you get the initial point. 7(a) loans can be a great vehicle for business acquisition or other projects that require large up front capital with a longer payback period.

Pros of the 7(a)

Typically have the lowest APRs available to most small businesses

Long term lengths (25 yrs for real estate, 10 yrs for non-real estate)

Monthly payments

Broad range of eligible uses and industries

Cons of the 7(a)

Weeks if not months before you receive funding

Lots of documentation - see the full list on the SBA’s website

Will often have higher credit requirements than other alternative term loan lenders

Strict collateral requirements including but not limited to personal RE assets

Variable rates can expose you to interest rate risk

Down payments (10-20%) - often not required by other alt-term loan lenders

Prepayment penalties

A Note on Prepayment Penalties

As previously mentioned, one of the benefits of a fully amortizing term loan is that making prepayments earlier in the term saves you more in total interest. However, the SBA does allow prepayment penalties negating some of this benefit.

For loans with a maturity of 15 years or longer, prepayment penalties apply when:

The borrower voluntarily prepays 25 percent or more of the outstanding balance of the loan.

The prepayment is made within the first three years after the date of the first disbursement of the loan proceeds.

The prepayment fee is as follows:

During the first year after disbursement, 5 percent of the amount of the prepayment.

During the second year after disbursement, 3 percent of the amount of the prepayment.

During the third year after disbursement, 1 percent of the amount of the prepayment.

So while there is an inherent benefit in the loan structure to prepay the lender ultimately loses out on that yield, which is why they often charge prepayment penalties.

Lenders

If you have an existing business relationship with your bank this is your best bet but make sure they are an SBA approved lender.

If you speak with your bank and they say you aren’t qualified then try with another lender, assuming you meet the minimum criteria outlined above.

If you still can’t find a lender, then you may want to explore other options. Check out my article on the SMB Lending Landscape to see what product might work best for your particular situation.

Conclusion

Well there you have it folks. As Deangelo Vickers says, “Thank you so much. Hope you learned something”

I really need to stop with all The Office references or I’m going to end up doxing myself.

As always, this is not financial advice. For educational and entertainment purposes only (do we really need to say this every time?).

-BTO