SMB Lending Market Update

SMB Lending Market Update

February 2023 Temperature Check

Summary

We aren’t even 2 months into 2023 and the SMB lending space has seen some interesting developments.

Is it too early to say shit is hitting the fan?

Probably.

But, there are some early indications of stress within SMBs and economic anxiety within SMB lenders.

2 big factors:

Demand for SMB loans remains strong

SMB lenders are tightening credit

Typically, these 2 developments happen in uncertain economic times.

Let’s walk through the recent developments.

Bluevine

Bluevine is a large player in the alternative lending space offering one of the more competitive line of credit products, outside of banks, in the SMB lending space.

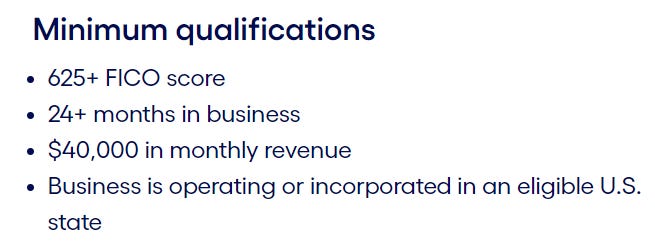

The year kicked off with Bluevine quietly updating their minimum qualifications.

I might have never discovered the change had I not been doing research for our post on the Best Small Business Loan Options

Bluevine made 2 pretty MAJOR changes:

Minimum time in business increased from 6 months to 24 months

Minimum monthly revenue increased from $10,000 to $40,000

A 4x increase in both factors. This is pretty significant.

There has been no news on the matter but to me this suggests some stress in their loan book. Nobody increases their requirements that much without seeing some delinquencies/defaults in that population of newer/smaller businesses.

It makes sense though. Businesses less than 6 months old and with revenue ~$120,000 typically aren’t the most qualified.

Additionally, Bluevine only requires the last 3 months of bank statements to underwrite their loans. Seems difficult to have any understanding of credit risk with such a limited amount of documents for underwriting.

Since there isn’t much info on this one, we’ll be keeping a close eye. Stay toon’d.

Upstart

Many may know Upstart ($UPST) as the stock darling that had a meteoric rise in 2020 & 2021 with an equally impressive 90%+ decrease in 2022.

Upstart is more known for their consumer lending, touting AI models that allow bank partners to increase approval rates with lower defaults. Though, it seems like that claim is now being tested (Source).

Upstart entered the SMB lending space in the Summer of 2022 and a quick 8 months later has already halted (Source).

Apparently it’s not as easy to make the switch from consumer to SMB lending.

We’ll see if Upstart attempts to re-enter the space once credit conditions become more favorable.

Credibility

Credibility is a large player in the alternative lending space offering one of the more competitive term loan products. Even with Credibility operating there weren’t many lenders offering term loans up to 5+ years with competitive bank/SBA-like rates.

This is a major blow to SMBs interested in term loans but ineligible for bank/SBA products. On the flip side, what a boon for other alternative term loan lenders. You can read more about term loans and the other lenders in our post: What are Business Term Loans?

Credibility, much like Bluevine, quietly updated their website, however we’re not sure exactly when.

The message on their application is somewhat cryptic and it remains unclear whether this is a temporary pause or Credibility is officially out of business.

We’ll be keeping an eye on this development and will keep our subscribers updated.

Plug: If you aren’t subscribed, SMASH that subscribe button NOW.

Enova

Subsidiaries Include: Ondeck, Headway Capital, & The Business Backer

Many of the direct lenders in the alternative SMB space are not public companies so understanding the market share of each is tricky. However, we do know Enova is one of the larger players in the space AND is a public company thus an important one to monitor to understand how SMB lenders are reacting to the economic environment.

David Fischer, CEO of Enova, offered some interesting insights on the SMB lending space during the company’s recent earnings call.

We are being very conservative with our small business lending right now. There’s a tremendous amount of demand […] I think both demand from businesses who need money coming out of COVID still but also from a lack of competition and a reduction of competition. So there’s a tremendous amount of demand. We’re filling a very small portion of it as we are trying to remain very, very conservative with respect to our originations, so we can manage through any turmoil in the economy.

Source: https://debanked.com/2023/02/enovas-current-small-business-lending-strategy/

If you operate in the space, like we do, than it’s not really any surprise that SMB loan demand is STRONG.

My take is that SMBs, much like consumers, got addicted to the free, pandemic-era government stimmies. They probably thought fiscal and monetary stimulus would last longer than it did and right when the government pulled back, inflation started taking off. SMBs were caught with their pants down, not enough money in the bank, and now rates are rising.

SMBs, much like consumers, are continuing to get beat up by inflation and it doesn’t seem like there’s an end in sight. And of course, right when it seemed like inflation was cooling, the January PPI report came out with higher than expected readings.

SMBs and consumers need cash because they never learn.

The irony is it’s really quite simple:

Live/operate below your means

Upgrade your skills/business to increase your earnings

Save and invest as much as you can

But apparently no one did that.

In response, many SMB lenders have tightened their lending criteria, as indicated by the numerous examples in this post.

Conclusion

Anyone with even a basic understanding of finance and economics understands that during tough economic conditions, 2 things happen:

Demand for credit increases

Supply of credit decreases

If that imbalance continues, it often exacerbates the underlying economic situation as businesses (and consumers) decrease their spending and, worse case scenario, go out of business leading to less demand and higher unemployment.

There seems to be a few predominant narratives currently out there:

Soft landing

Inflation and rates continue increasing leading to a short but quick recession as the Fed quickly lower rates

Higher inflation and rates persist leading to a sluggish recovery

Nobody actually knows. Anyone who says they do is probably not to be trusted.

As always, this is not financial advice. For educational and entertainment purposes only.

Smash that share button and post on Twitter to spread the word of BTO.